7 Reasons Why You Should Retire Early

Who doesn’t want to retire early? Let’s talk about 7 reasons to retire as quickly as you can.

BREAKING NEWS: Life is short.

That one’s a shocker, right?

Most people don’t consider retirement to be an option until their 60’s.

A 2024 Mass Mutual survey found that the average retirement age in the US was somewhere around 62-63.

The biggest reason for this is because Social security benefits are not able to be claimed until one reaches the age of 62. Although, it’s worth noting that electing to receive social security benefits at age 62 will greatly reduce one’s full retirement age benefit, which is usually attained when claiming at 66 or 67. For this reason, claiming early is often not advisable.

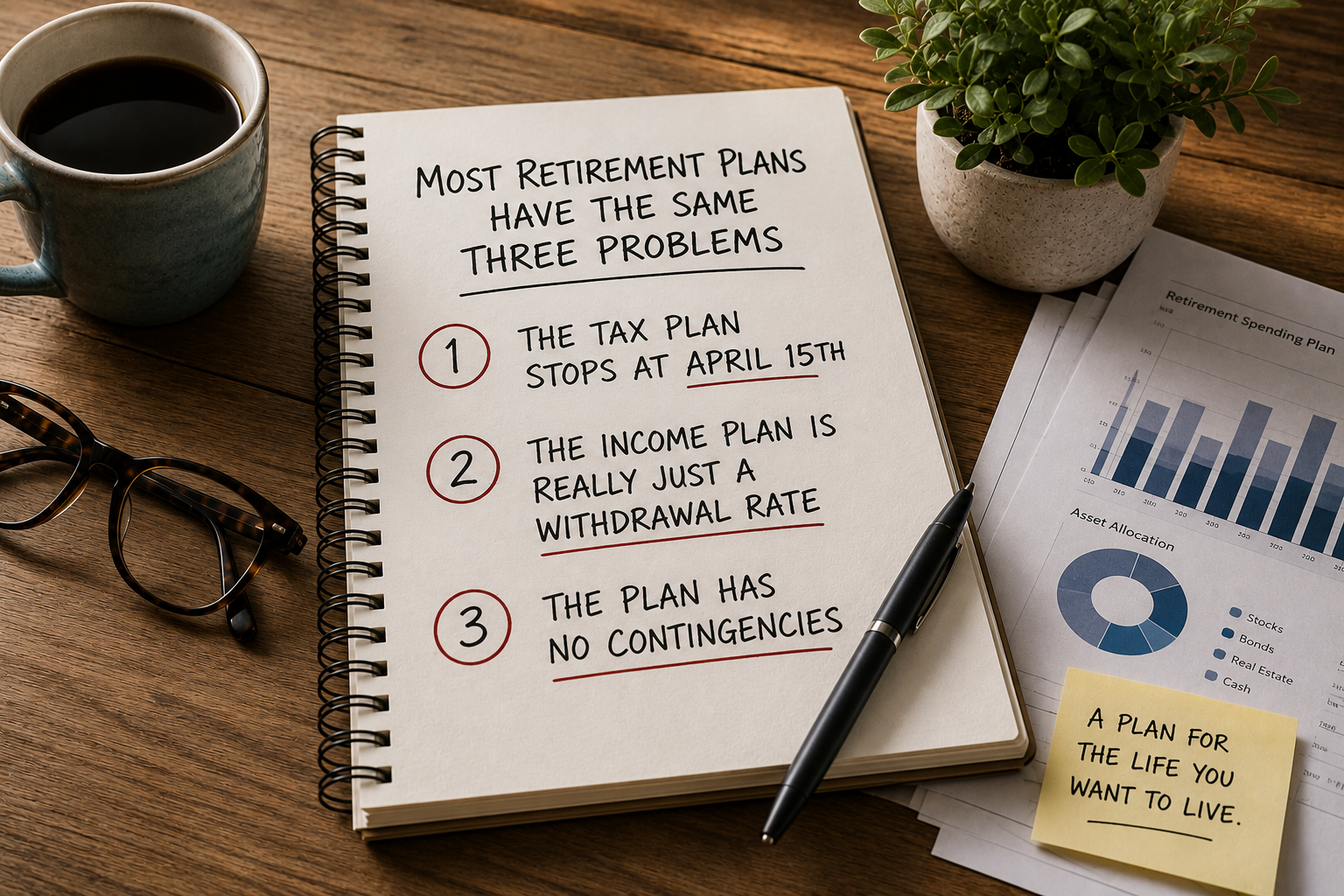

In life, our biggest constraints are generally time, health, and money.

The older we get, the more we care about time and health and the less we care about money beyond what’s needed to support our basic living needs.

So, lets talk about seven good reasons to consider stepping away from work sooner rather than later:

The Seven Reasons:

1. Time is Just “Too” Valuable

As we age, we start to realize how quickly time goes by.

This is in large part to how we perceive time.

When you’re 10 years old, a year is 10% of the life that you have experienced thus far. That’s quite a lot.

As a 50 year old, it represents just 2%. Not so much.

Every year that we age, is a smaller portion of the life we have lived, causing us to perceive time as “speeding up”.

If you're 55 and ambitious about making it to 90, you would have 35 more holidays, annual trips, summers, etc., as visualized by the below chart. (We’ll, that’s depressing, Charles!)

Retiring earlier allows you to increase the purple shading and decrease the red shading, so that you have more of these meaningful moments on your own time while you're still vibrant and active.

2. Your Health Won’t Wait..

Most people’s retirement dreams often involve travel, hobbies, and new adventures.

These dreams are typically demanding enough that they require fairly good health and mobility.

The earlier years of retirement are usually the healthiest—physically and mentally.

Waiting too long to retire could mean missing the window to truly enjoy the years in which you are physically able to do all that you have been delaying.

3. Work Is No Longer Enjoyable

Point #3 assumes that you enjoyed your job or career at some point in the past, which hopefully you can attest to. My strong opinion on this is that most of us work far too much of our lives (see above chart on time) working to not somewhat enjoy what we do.

As people reach the tail end of their working years, they can begin to feel drained and deprived of a connection to their work.

It feels more like a routine than a passion. If your work no longer excites or challenges you, or if it’s starting to wear you down, it could be a signal that it’s time for something new.

Many who retire earlier than planned find themselves feeling lighter, happier, and more fulfilled once they step into a new rhythm of life.

Now, what’s very important is defining what you are retiring “to” and not just what you are retiring “from”. I’d encourage you to take your time exploring new hobbies, groups, and communities so that you can identify what excites you about your next chapter.

4. You Want More Control in Life

This one ties in very well with the first three.

You have been trading your time for money for decades, relinquishing a lot of control over how you can live and operate within society.

At some point, you may want that control back.

Whether that’s fully retiring, consulting, volunteering, or just having more freedom in your day-to-day life, earlier retirement puts you back in control of your schedule.

When you're no longer living around the demands of a job, you can design your life around what brings you energy, purpose, and joy.

5. There is No “Right” Time

I find that a lot of people delay retirement because they don’t think now is the “right time” because:

The stock market is too volatile

The economy

The current administration

They don’t want to leave their employer high and dry

In reality, there is never a “perfect” time to retire. The markets move up and down every day. The economy has its ebs and flows.

However, if you have a well-built retirement plan, you don’t need to wait for “perfect” conditions. If anything, waiting too long can cost you a lot.

6. Your Retirement Goals Have Become Arbitrary

It is very common to see people with big-picture retirement “goals”, such as retiring at 65 or accumulating $1 million or $5 million.

The problem is that these goals aren’t specific enough, nor are they usually captured within your retirement plan.

When people peg to these arbitrary goals, it becomes too easy for them to just “work one more year” or “save another X dollars”.

More important is to detail what’s important about your future to you and encapsulate this into your retirement plan, so that you can identify your point of financial freedom.

7. You Might Be Able to Retire and Not Know It

A lot of retirement advice is built on general rules: save 25x your expenses, retire at 65, withdraw 4% a year, accumulate $1 million or $2 million.

However, personal finance is “personal”, and these rules do not incorporate the nuances of your life.

-Maybe your expenses will drop significantly.

-Maybe you’ll downsize.

-Maybe you’re willing to spend more in your early years and scale back later.

For example:

You may want to retire on $7,000/ mo. of income indexed every year for inflation.

Traditional rules, such as the 4% safe withdrawal rate would suggest that you need $2.1 million to safely withdraw $7,000/mo. (or $84,000/yr.) from your investment accounts over a 30-year retirement without running out of money.

This assumes that your spending stays at a steady $7,000/mo. forever.

In reality, retirement spending typically looks like a “smile”.

Retirement Spending Smile:

Go-Go Years (Early Retirement): Early one, you spend more on discretionary things like travel and big purchases.

Slow-Go Years (Mid-Retirement): Your spending goes down as you age and settle into retirement.

No-Go Years (Late Retirement): Discretionary spending drops off but overall spending tends to rise due to costs associated with aging and chronic conditions.

Also, you have to incorporate your other sources of dependable income like social security, pension income, real estate income, etc.

Given this guaranteed income, you may need to save less than you think.

Not So Fast!

This is an article on why you should retire as soon as feasibly possible.

However, there are also reasons to continue working even if you have reached the point of financial freedom.

If work remains purposeful and you don’t mind the time tradeoff, then continuing to work may be a great idea.

Hopefully, these seven reasons gave you new perspective and caused you to pause and reflect on the journey that you are on.

Have any questions about what you’ve read? Let’s talk about them!

Read My Other Work!