The Problem with Most "Financial Advisors"

Why the conventional “financial advisor” tends to fall short of what people actually need and deserve.

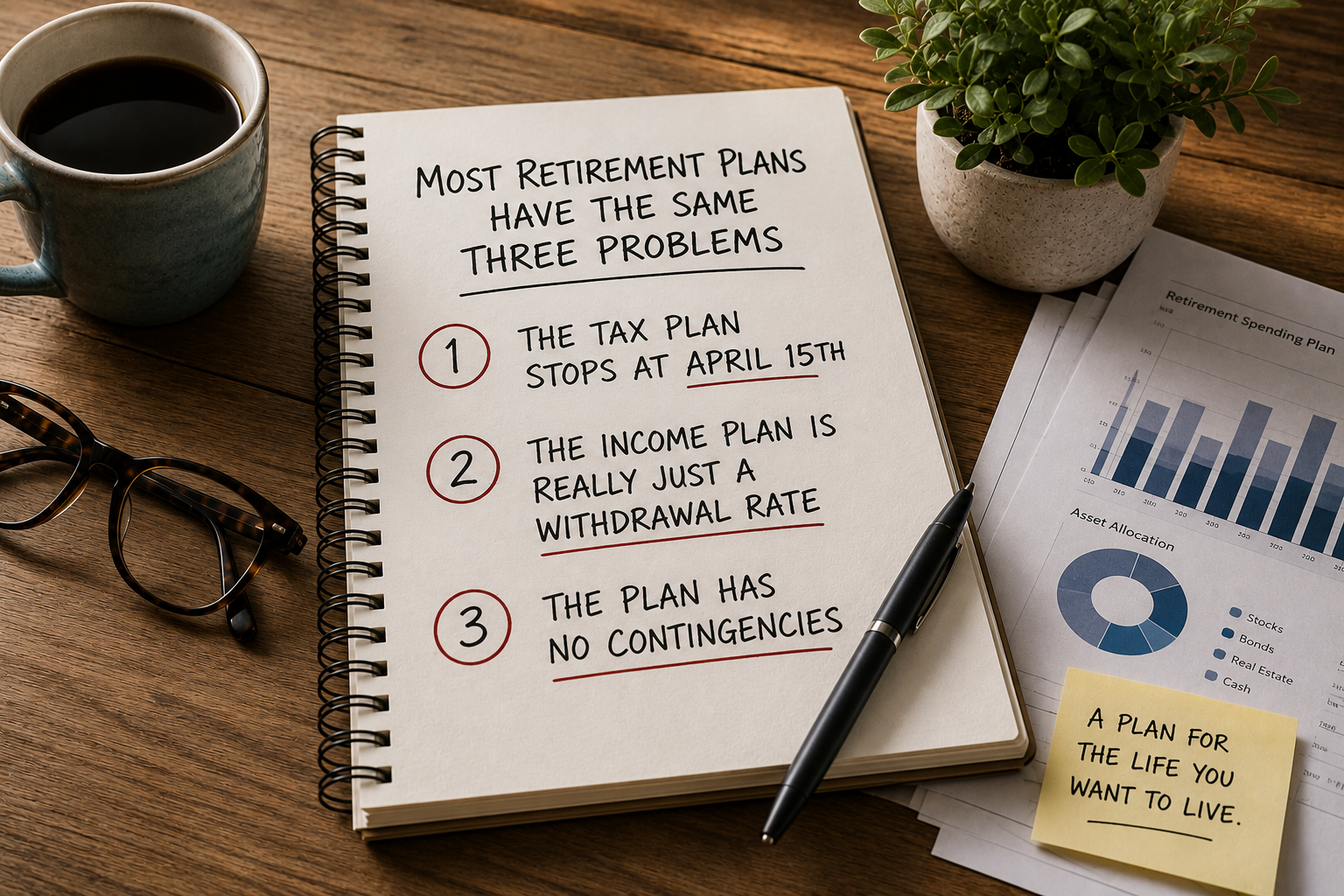

Help Me Understand This!

Unfortunately, not all financial advisors are created equally.

The term “financial advisor” is not a regulated title. Anyone can call themselves one, whether they work at a life insurance company, a bank, a shop on the corner, you name it. What’s unfortunate is the title itself is often diluted by those practicing in a “less than ideal” manner without regard to quality, sound financial advice that’s best for their clients. Let’s break this down..

The Typical "Financial Advisor"

The sad reality is that most “financial advisors” in the financial services industry function primarily as salespeople rather than advisors. Their business affiliation and compensation models incentivize them to place you in investment funds and insurance products that pay them the biggest kickbacks. While these investments and products can play a role in your financial plan, this sales-driven approach can be predatory and neglect your broader financial needs. Here’s what you need to know about financial salespeople:

Heavy Investment & Insurance Focus: Their recommendations often revolve around investments and insurance aka products, with limited regard for your overall financial picture. They may so “light” financial planning but its typically fairly basic in scope.

Commission-Based Compensation: These advisors earn money fully or in part through commissions or bonuses tied to the products they sell, creating a potential conflict of interest.

Lack of Comprehensive Planning: Financial salespeople rarely provide full picture advice. Areas like tax strategy, cash flow management, and estate planning are often ignored, leaving gaps in your financial life.

Short-Term Focus: Because their compensation is linked to sales, these advisors may prioritize immediate transactions over your long-term goals.

The Real Financial Planner

In contrast, a smaller group of financial professionals operate as true financial planners. These individuals take a 360 degree, purpose-driven approach to your money. Their goal isn’t just to manage your money but to help you align it with what’s important to you. Here’s how they typically stand out:

Comprehensive Planning: True financial planners don’t just focus on investments or insurance. They provide guidance across all aspects of your finances, including retirement planning, tax strategy, cash flow optimization, estate planning, and more.

Tax-Smart Decision-Making: These advisors prioritize strategies that minimize your lifetime tax picture and maximize your wealth. From Roth conversions to capital gains management, they integrate tax efficiency into every financial decision.

Fiduciary Responsibility: Real financial planners typically operate under a fiduciary standard, meaning they are legally required to act in your best interest. This eliminates conflicts of interest often seen with commission-based advisors. Caution: The difficulty with this is that most financial advisors call themselves “fiduciaries” even if they’re not.

Values Alignment: They take the time to understand your unique goals, values, and purpose, ensuring that every recommendation helps you achieve what truly matters to you.

Collaborative Approach: Real financial planners often work in close coordination alongside your other professional advisors like accountants, attorneys, etc., to ensure every aspect of your financial life is aligned and that there are no gaps.

The Difference Visualized

I love showing the below graphic that Fidelity puts out on what model financial advice looks like because it’s so good and telling.

Financial salespeople will typically focus on the left half of the “Managing the Money” row (Money Manager Selection to Insurance"). They may help with a bit more than that and give you some light goal planning (retirement, college planning, etc.) but it’s usually fairly basic.

Real financial planners consider the bottom two rows of the pyramid as table stakes. It’s the bare minimum that a halfway decent advisor does for their clients.

However, the great ones go beyond this in an effort to allow their clients to move up this pyramid into the “Peace of Mind” and “Fulfillment” rows.

P.S. Here’s how I practice!

Finding Quality Financial Planners

Here are some of my favorite questions to ask of your current financial advisor or of the ones that you interview in the future:

What are your credentials? An advisors credentials can tell you a great deal about their education levels and expertise. Remember, “financial advisor” is not indicative of any formal training or education. The most respected industry credential is CFP® (CERTIFIED FINANCIAL PLANNER™).

How are you compensated? Look for fee-only advisors who charge a flat fee, hourly rate, or percentage of assets under management. This structure reduces conflicts of interest tied to transaction-related commission oriented selling.

How do you ensure that you are providing advice best suited to your clients with minimal conflicts of interest? This ties in with the last question.. If a client is affiliated with a bank or insurance company they will likely have inherent conflicts in their compensation structures and products that they will be motivated to recommend. The advisor should be articulate in the answer to this. Advisors at independent firms tend to have the fewest conflicts of interest.

What financial planning areas do you cover? Seek an advisor who offers comprehensive financial planning, including tax strategy, retirement planning, cash flow management, and estate planning.

What does your typical client look like? This question will give you insight into how well equipped the advisor is with handling clients situations like yours.

Additional Tip #1: You can find more great information and questions with Charles Schwab’s free “How Do I Choose the Right Advisor” brochure found here.

Additional Tip #2: Search the advisor on this site that the SEC publishes. This can tell you relevant information about the advisor and their current registration. You can also see if they have any client disclosures which can often be a red flag.

Have any questions about what you’ve read? Let’s talk about them!

Read My Other Work!