Retiring in 10 Years? Do These 10 Things!

You've dedicated decades to your career, dreaming of the day of no more “work” and a life that you have ultimate control and flexibility over. You’ve delayed fun to raise your kids and save for retirement but now it’s time to start thinking about “landing the plane” on your “retirement runway”.

But, HOW in the world do you do this?

It’s no surprise that the decade leading up to retirement is crucially important.

Now is the time to measure twice and cut once to ensure that you’re not only financially able to make this transition but that you’ve identified your purpose and vision for retirement. I like to call this your “retirement why”.

Let’s get into my 10 things to do in the 10 years leading up to retirement.

1. Start With Your “Retirement Why”

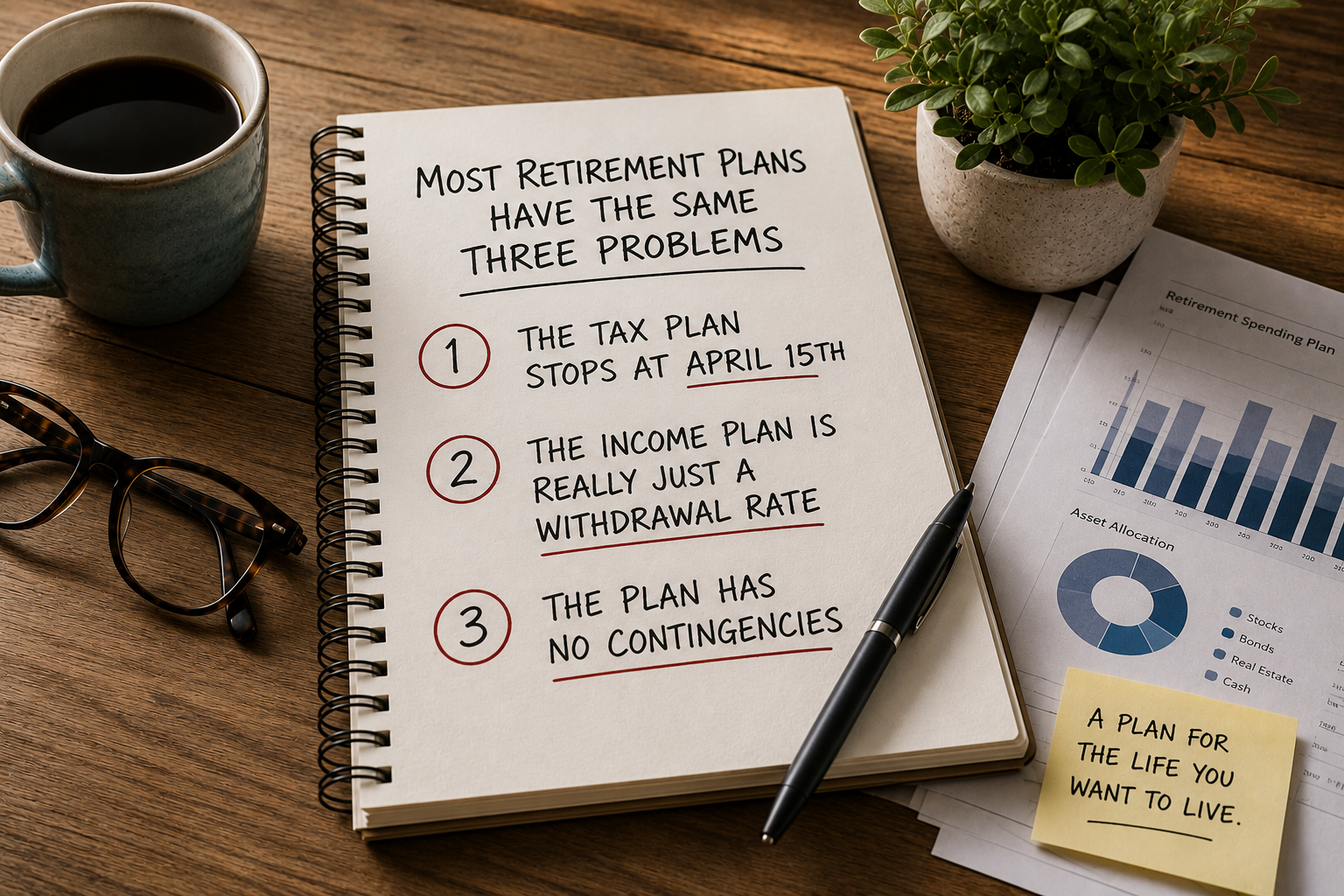

Most people will start by focusing on a magic retirement “number”. Something arbitrary like ten times their last year’s salary or something they heard their neighbor or Dave Ramsey say (please tune out people who don’t know the ins and outs of your life).

Before we even get to thinking about how much it will take to live the life you want, you have to think about the life you want! It is paramount that you begin visualizing what you will be retiring “to” and not just dwelling on what you’re retiring “from”. I challenge you to try new hobbies, join that local non-profit, get involved at your church; do something to shake up your routine.

For those who really struggle with this, I came across something really interesting that Chip Conley, American hotelier, entrepreneur and author, created. It’s called Modern Elder Academy (M | E | A). They call themselves “the world’s first midlife wisdom school”. Essentially, it’s a program that you can join to find that spark and renewed passion or calling that might be missing from your life. The program combines online learning with destination workshops where you can meet others and is something you have to check out!

2. How Much Will You Need Per Year?

Now that our creative juices are flowing and we’re thinking about what’s important to us in our next chapter, we need to consider what it will cost. How much money per year will it take to live the retirement you want? You will need to account for housing, healthcare, travel, hobbies, daily living costs, etc. Many retirees underestimate discretionary spending early in retirement when they are most active and healthcare expenses in their later years.

Note: Some expenses may drop off in retirement, like a mortgage or support for children, so don’t forget to account for those things.

3. Build or Update Your Financial Roadmap

With the help of a CERTIFIED FINANCIAL PLANNER™ professional, build or update your financial plan.

The plan will incorporate your vision, what you currently have, what you will need and to live the way that you want to in retirement.

Want to model spending $100,000/yr instead of $75,000/yr? The plan will model this. Want to step away from work at 62 instead of 65? The plan can illustrate the impact of this.

4. Review Your Portfolio and Investment Strategy

Given what your financial plan indicates, there may be shifts warranted in how you’re currently invested and how you ought to be from a risk capacity and tax efficiency perspective.

You’ll want to make sure that that your investment strategy is one that you can stick to through good and bad times in the market and that your portfolio is positioned to grow beyond inflation while effectively managing risk.

Your portfolio needs to be able to support this shift from accumulation during your working years to distribution during retirement, so please measure twice and cut once with regards to configuring your portfolio.

5. Boost Your Retirement Account Savings

Use your plan as a guide to help you decide what your retirement account funding should look like in your last working decade. Your plan may say that you’re ahead of schedule and that further increases in retirement savings are not necessary or it might identify the need to catch up and increase your retirement savings rate.

Reminder: If you are over the age of 50 in 2025, you may contribute $31,000 as an employee deferral contribution to your 401(k)/403(b)/457(b), etc. and $8,000 to IRAs.

Note: You may be able to contribute more to your employer plans with “after-tax” contributions if your plan allows for it.

New in 2025: Starting in 2025, if you are between the age of 60-63, you may contribute an additional $3,750 as an employee deferral contribution to your employer sponsored plans, for a total of $34,750.

6. Evaluate Social Security Timing

Deciding when to claim Social Security is crucially important. You are entitled to your full benefit at “Full Retirement Age” (FRA) which for most people is around their age 67.

Taking benefits earlier than 67 can result in a decrease in lifetime benefits by ~8%/yr. and a similar story is true for delaying benefits until age 70 (Benefits increase 8%/yr.).

Your optimal social security timing strategy will be based on your expected longevity, the discrepancy between you and your spouse’s benefits, your other retirement income and assets, etc.

7. Plan to Minimize Retirement Tax Bill

I talk about this a lot with my clients and in my publications. Very few people are engaging in continuous tax planning with their advisor and accountants to ensure that they are paying the least amount of taxes possible over their lifetime. Most people fixate on what happened last year, what is happening this year and what might happen next year. You have to take a wider lens when reviewing your tax plan so that you have control over as many levers as possbile.

See my blog post on “Why Your Retirement Taxes Might Go Up—and What to Do”.

8. Plan for Healthcare & Long-Term Care

Medicare eligibility begins at 65, but it doesn’t cover everything. Explore supplemental insurance (Medigap), long-term care insurance, and Health Savings Accounts (HSAs) while you’re still working.

Long-term care is being needed by more and more people in their later years, so if you do not have long-term care insurance (and it’s too expensive to obtain today), you must build a sufficient buffer of funds (six figure cost for 2-3 years inflated at 4-5%/yr., as a starting point) into your financial plan.

9. Evaluate Your Debt and Emergency Reserves

Are you debt-free? If not, what debt do you still hold? You might want to keep around your mortgage payment as long as possible given a favorable interest rate or maybe psychologically, you would like to be rid of it. At a minimum, you’ll want to clear the table of all high interest debt obligations.

Having an appropriate emergency reserve in retirement can put you at ease if emergency expenses come up or if the stock market is in turbulent times. I’d aim for one year of your retirement expenses in something liquid like a money market fund or high-yield savings account that is paying an attractive rate.

10. Revisit Your Estate Plan

Last but not least, everyone’s favorite, estate planning.

Ensure your will, trusts, powers of attorney, and beneficiary designations are up to date. Estate planning is crucial for protecting your wealth and ensuring a smooth transfer to heirs or charitable causes.

Remember: Beneficiaries listed on retirement accounts, insurance policies, etc. pass directly to those people without the involvement of your will. It is important that these designations are coordinated with your other estate planning wishes. Also, if you have a trust make sure that it is funded! An unfunded trust is pointless and ineffective.

Have any questions about what you’ve read? Let’s talk about them!

Read My Other Work!