Which Accounts Should You Withdraw From First in Retirement?

When you're working, it’s pretty straightforward how you get paid.

A paycheck shows up every two weeks or every month, and that’s what you live on.

However, it’s not that simple in retirement!

Your paycheck stops, but your need for income doesn’t.

Suddenly, you’re left to create your own.

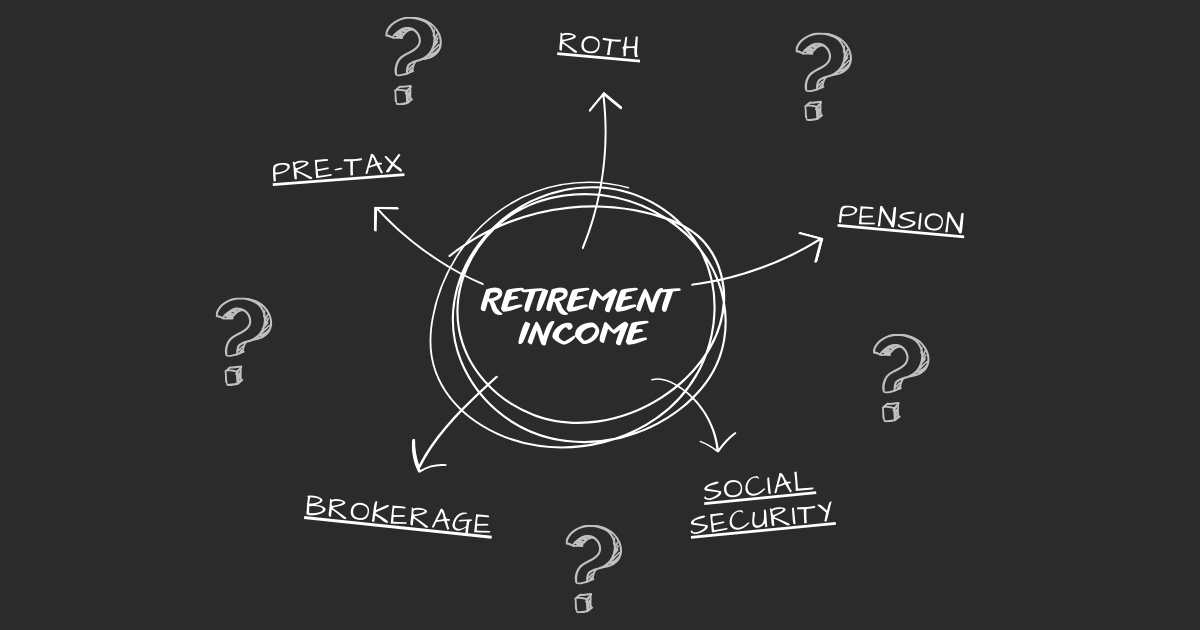

You may have accumulated balances in several different types of accounts.

1) Pre-tax retirement accounts

2) Roth accounts

3) Brokerage accounts

In addition, you may also receive income from sources like Social Security or a pension.

Among all these options, how do you decide which source to tap and when to fund your retirement life?

This is one of the most important (and misunderstood) parts of retirement planning.

The withdrawal order you choose affects how long your money lasts, how much you pay in taxes, how large your Medicare premiums are, and even what your heirs eventually receive.

And the research is clear: withdrawal order matters just as much as withdrawal rate.

The Traditional Rule of Thumb: Taxable → Tax-Deferred → Roth

The most common advice you’ll hear is that you should withdraw from your accounts in this order:

Taxable accounts first

Tax-deferred accounts (IRAs, 401(k)s) next

Tax-free Roth accounts last

This approach generally works because:

Taxable accounts often produce lower tax drag early in retirement

Pulling from IRAs too early can push you into higher brackets unnecessarily

Letting Roth money grow longer allows tax-free compounding

Each dollar left in a Roth becomes more valuable the further out you go

This sequence often reduces lifetime taxes and extends portfolio longevity, assuming steady income needs.

But the story doesn’t end here.

Why Other Income Sources Change the Strategy

Social Security and pensions don’t simply add to your income; they reshape your tax landscape.

Social Security becomes partially taxable depending on how much other income you have.

Pensions behave like wages and can lift you into higher brackets.

Required IRA withdrawals later in life can stack on top of Social Security, sometimes unexpectedly raising taxable income.

This means your withdrawal strategy can’t exist in a vacuum. It has to be coordinated with when you claim Social Security, how much pension income you receive, and how your taxable, pre-tax, and Roth accounts interact with that baseline income.

A withdrawal plan that ignores these sources often leads to higher taxes, higher IRMAA surcharges, and fewer planning opportunities.

A Better Withdrawal Strategy?

A more effective withdrawal plan often includes an extra step that many retirees miss: using your low-income years in early retirement to complete strategic Roth conversions.

When you stop working, your income typically drops from where it was before retirement, as evidenced by the diagram below.

This opens a valuable window, often the period after you stop working but before Social Security and other income sources begin. This creates an unusually favorable tax environment to exploit.

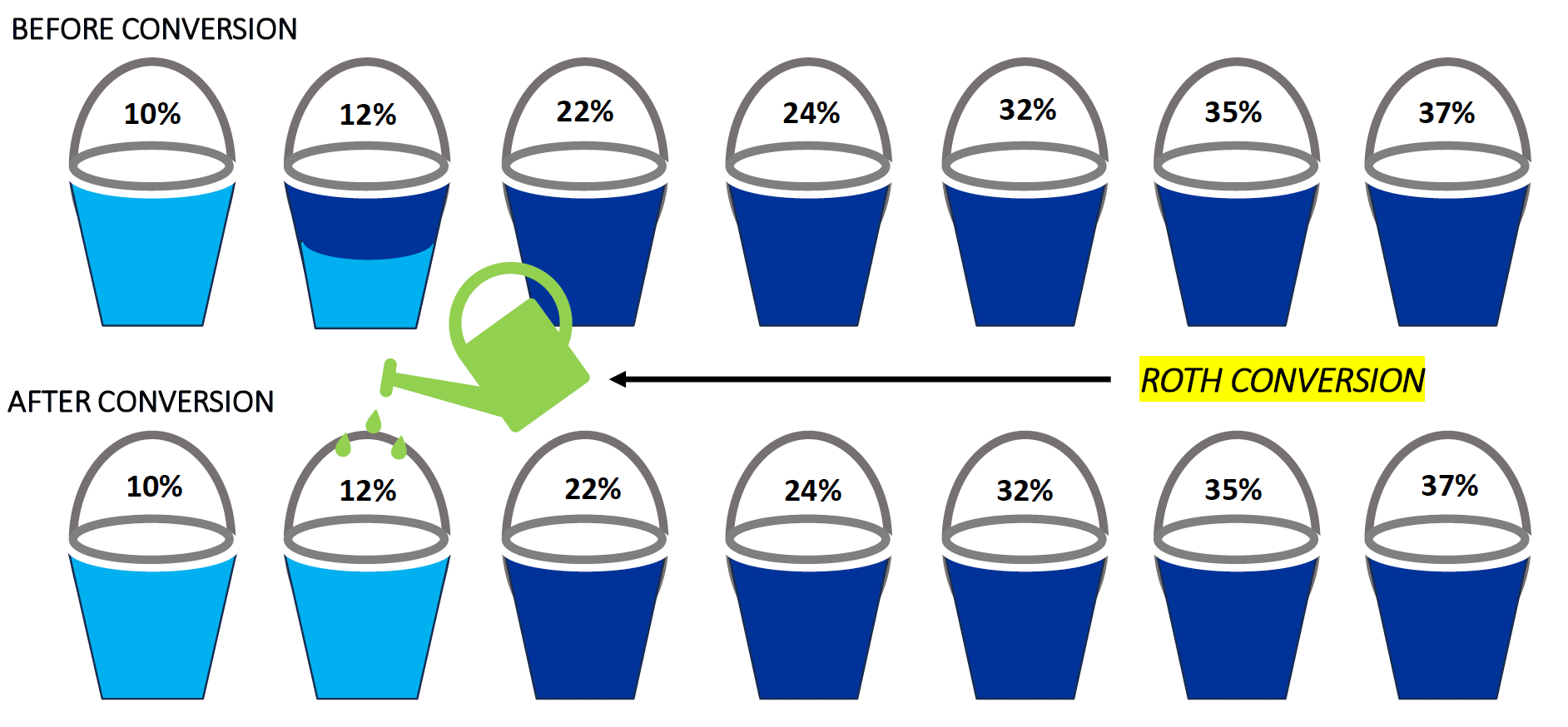

Your taxable income may be the lowest it will ever be again, which means you can convert portions of your traditional IRA into a Roth at comparatively low tax rates.

You might find yourself sitting comfortably within the 12% federal tax bracket today, yet see a future where your income pushes you into the 22% or 24% brackets.

That gap creates an opportunity: converting enough IRA dollars to “fill up” the 12% bracket now allows you to pay tax at today’s lower rate rather than tomorrow’s higher one.

By doing this steadily over several years, you shrink the size of your future tax-deferred balances, reduce the tax drag later in retirement, and give your Roth accounts more time to grow tax-free.

This one adjustment can meaningfully improve your lifetime tax picture and create far more flexibility in how you withdraw money in your 70s, 80s, and beyond.

Withdrawal Order Isn’t One-Size-Fits-All

The research consistently shows that rigid rules, like always spending taxable first or Roth last, rarely produce the best result.

The most effective withdrawal strategies are dynamic.

They are tailored to:

Your marginal tax bracket

Your Social Security timing

Your account balances

Market performance

Medicare thresholds

Your goals for legacy or gifting

For most retirees, the optimal path is a thoughtful blend of taxable, tax-deferred, and Roth withdrawals, with a focus on minimizing lifetime taxes, not just the taxes you owe today.

Have any questions about what you’ve read? Let’s talk about them!

Read My Other Work!